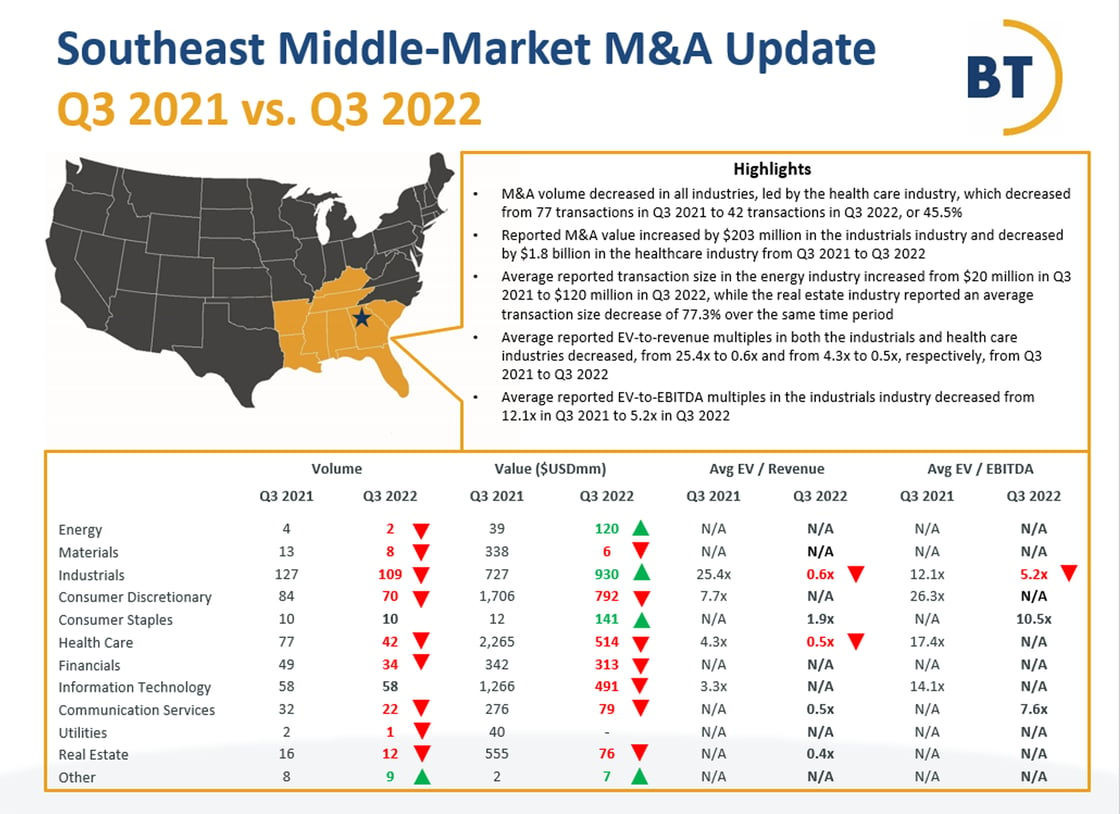

In this Q3 2022 update, we provide data and highlights for Southeast (Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Mississippi, South Carolina and Tennessee) middle-market (total transaction value < $USD 500mm) M&A transactions, including volume, value and enterprise value multiples. This update focuses on M&A trends in the energy, materials, industrials, consumer discretionary, consumer staples, health care, financials, information technology, communication services, utilities and real estate industries.

Currently ranked among the largest CPA firms in the US, Bennett Thrasher is a premier provider of professional tax, assurance, consulting and wealth management services to businesses and high net worth individuals. Since 1980, our integrity has earned our client’s trust, and our culture of supporting professional and personal growth has created a long-term, dedicated team.

Speak to one of our professionals today to learn how we can be Better Together.

Highlights

Total M&A volume decreased by 21.5%, from 480 transactions in Q3 2021 to 377 transactions in Q3 2022, largely driven by a 45.5% decrease in the health care industry, from 77 transactions in Q3 2021 to 42 transactions in Q3 2022

Total reported M&A value decreased by 54.2%, from $7.6 billion in Q3 2021 to $3.5 billion in Q3 2022, mainly due to a substantial decrease in the health care industry, from $2.3 billion in Q3 2021 to $514 million in Q3 2022

Average reported transaction size decreased by 15.3%, from $89 million in Q3 2021 to $75.4 million in Q3 2022

Average reported enterprise value (“EV”)-to-revenue multiples decreased from 9.9x in Q3 2021 to 0.7x in Q3 2022

Average reported EV-to-earnings before interest, taxes, depreciation and amortization (“EBITDA”) multiples decreased from 19.2x in Q3 2021 to 7.8x in Q3 2022

Q3 2021 vs. Q3 2022

Volume, Value and Average EV Multiples

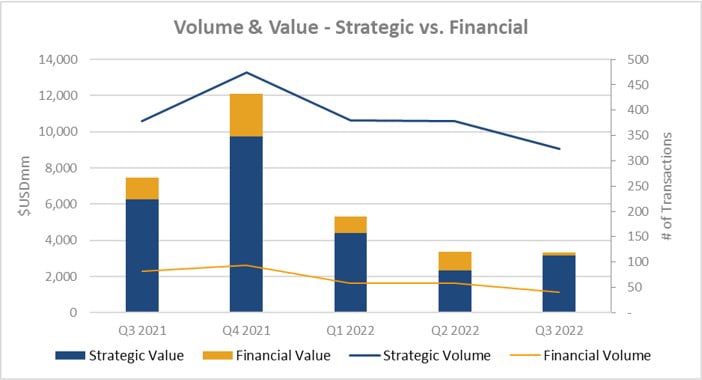

M&A volume involving both strategic and financial buyers decreased from Q3 2021 to Q3 2022, from 378 transactions to 324 transactions (14.3%) for strategic buyers and from 82 transactions to 41 transactions (50.0%) for financial buyers

Reported M&A value involving both strategic and financial buyers decreased from Q3 2021 to Q3 2022, from $6.3 billion to $3.2 billion (49.6%) for strategic buyers and from $1.2 billion to $183.6 million (84.6%) for financial buyers

Average reported transaction size involving both strategic and financial buyers decreased from Q3 2021 to Q3 2022, from $94.8 million to $83.1 million (12.4%) for strategic buyers and from $70 million to $30.6 million (56.3%) for financial buyers

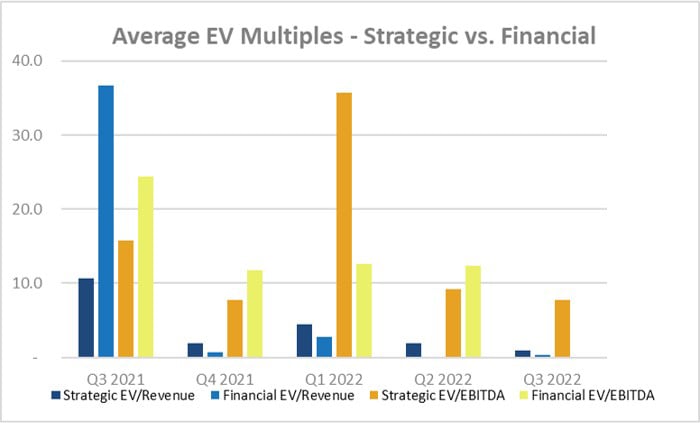

Average reported EV-to-revenue multiples for transactions involving both strategic and financial buyers decreased from Q3 2021 to Q3 2022, from 10.7x to 1.0x for strategic buyers and from 36.8x to 0.3x for financial buyers

Average reported EV-to-EBITDA multiples for transactions involving strategic buyers decreased from 15.7x in Q3 2021 to 7.8x in Q3 2022

Better Together Spotlight: Sell-Side Due Diligence Services Assist Healthcare Client in Private Equity Recapitalization

Bennett Thrasher recently assisted a client in the healthcare sector with sell-side due diligence related to a recapitalization they were seeking by private equity. While the management team and the accounting function were both fairly sophisticated, the company had never been audited before. The company’s investment bankers strongly recommended a quality of earnings analysis be performed and Bennett Thrasher won the bid. Healthcare deals are highly complex and require specialized technical knowledge of revenue recognition specific to this vertical. Absent this approach, sophisticated healthcare investors can often find meaningful differences in the revenue and earnings reported, which can adversely impact the valuation of a company and/or cause broken deal processes. Through our quality of earnings analysis, we performed a deep-dive on the billing and collection cycles in conjunction with revenue recognition. Based on our analysis of when performance obligations were met, we recommended a change to the revenue recognition process. We used the data made available internally and adjusted the company’s revenue recognition by comparing dates of payment and dates of service to the date the performance obligation was met. The results of our analysis involved a recalibration of revenue to more appropriately reflect accrual basis expectations through our cash collection waterfalls and related analyses. The time and effort spent on the front end resetting revenue recognition and thoroughly documenting the rationale for the change and the methodology used allowed the client and banker to avoid any pushback on the adjusted revenue proposed. We presented our analysis to three private equity bidders post initial indications of interest and discussed with their respective buy-side due diligence teams, all of whom agreed with our revenue recognition approach. This prevented any re-trading during the diligence process and allowed for a timely and successful close of the transaction leaving all parties involved satisfied with the results.

Our M&A Advisory Services

For most business owners, a merger or acquisition is the most significant financial event of their lifetime. Buyers and sellers face many hurdles in reaching their goals of maximizing business value and minimizing risk. The experience of transaction advisors can be instrumental to achieving these goals.

Our team is comprised of dedicated advisors that can assist you across various stages of your transaction process, including:

Financial due diligence

Tax due diligence/structuring and valuation

Sell-side readiness

Exit planning

If you are embarking on a transaction opportunity, please contact one of ourM&A Advisory Servicesleaders by calling 770.396.2200.